The property game in Australia may be changing forever

The property game in Australia may be changing forever.

For years Australians were conditioned to believe property only goes one way.

Buy it.

Hold it.

Watch it go up.

But markets evolve.

And right now we have a perfect storm forming underneath the surface:

Higher interest rates

Federal budget changes

Lending constraints

Affordability pressure

Rising construction costs

Slowing buyer demand

Investors becoming more cautious

Consumer confidence is low

The result?

Property price growth is likely to weaken further, with more markets potentially experiencing declines.

Now importantly, this doesn’t automatically mean a property crash.

Most homeowners still have strong equity positions (loans are much lower than the value of the home) and savings buffers.

So any slowdown is more likely to come from softer demand rather than a flood of forced selling.

And that’s a very important distinction.

One of the biggest changes people are underestimating is lending.

Most people think negative gearing is simply a tax refund at the end of the financial year.

But lenders actually use those projected tax benefits upfront when calculating borrowing power.

That means if negative gearing rules change, borrowing capacity changes too. We are now seeing lenders already adjust their servicing to reflect the potential changes.

And some estimates suggest investors could see borrowing power reduce by 15%–25%.

That’s huge.

A 20% reduction in borrowing capacity can be the difference between buying in the suburb you want…

or being completely priced out.

And this is happening while rates are already high.

Historically, every 0.50% increase in rates has reduced borrowing capacity by roughly 5%.

So investors may now be facing a double hit:

Higher assessment rates from lenders

Reduced servicing benefits from negative gearing

Then layer on global uncertainty, higher living costs and mortgage stress.

The pressure starts building.

According to recent data, dozens of capital city postcodes are already seeing higher levels of mortgage stress and increased default risk.

In simple terms?

Many households are now spending more than they bring in.

Some are using credit cards just to keep things moving.

Others are quietly kicking the can down the road hoping rates fall soon.

That’s where confidence starts getting chipped away.

At the same time, the government is clearly trying to encourage new builds by preserving the old negative gearing treatment for newly built properties.

But even that comes with challenges.

Construction costs are already up roughly 17–18%.

And some forecasts suggest building costs could still rise another 10–18% from here.

So yes, new builds may become more attractive from a tax perspective…

but they’re also becoming more expensive to deliver.

Now here’s the part I think matters most.

The easy money phase of property feels like it’s fading.

And the leading indicators are starting to show it.

One of the best indicators in property isn’t the headlines.

It’s auction clearance rates and time on market.

Clearance rates measure the percentage of properties that sell at auction.

Higher rates suggest strong buyer demand, while lower rates point to a softer market.

I was speaking to a real estate agent recently who said:

“six months ago I was selling these in under two weeks. Now they’re sitting for 2 months plus.”

That says a lot.

Last week’s auction data tells a similar story.

Sydney clearance rates came in at 43.1%.

Melbourne was 54.4%.

Brisbane dropped below 50% at 49.7%.

Combined capitals are now sitting around 50.4%.

That’s a very different environment compared to late last year when many areas were seeing 70%+ clearance rates.

Clearance rates show real buyer demand in real time.

Buyers either step up…

or they don’t.

Prices are lagging indicators.

Clearance rates are leading indicators.

What we’re seeing now is buyers becoming far more selective.

Agents are having to work harder.

Sellers no longer hold all the negotiating power.

And the environment where almost anything sold quickly is fading.

There will still be outperforming areas.

There always are.

But broad-based easy gains across the entire market?

That environment is changing.

Now zooming out even further…

The government is also trying to balance two competing problems:

Housing affordability

Economic growth

And immigration sits right in the middle of that discussion.

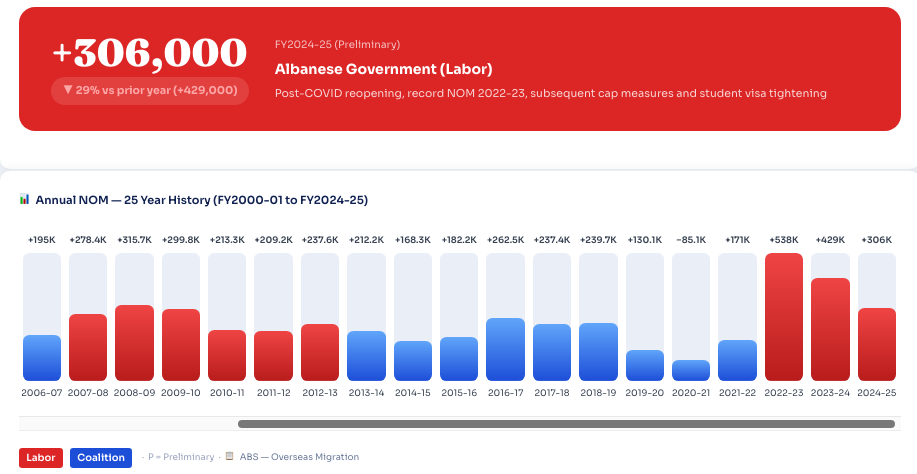

Below shows the how each Government shaped immigration net overseas migration (NOM) since 2006/2007

Why do governments love immigration?

Because it creates immediate economic activity.

More workers.

More specialised skills.

More taxpayers.

More housing demand.

More spending.

But if housing supply can’t keep up, pressure builds quickly.

That’s why I believe the next phase of property investing won’t simply be about “buying property”.

It will be about:

Buying quality assets

Understanding structure

Managing cash flow

Knowing the tax rules

Being selective about location and demand

The investors who do well over the next decade likely won’t be the people chasing hype.

They’ll be the ones making calm, strategic decisions.

One quote I love fits perfectly here:

“When the tide goes out, you see who was swimming without shorts.”

Easy markets hide bad decisions.

Balanced markets expose them.

If you’re wondering how these changes may impact your property plans, borrowing power or investment strategy, contact us or SMS 0483 937 777 with “PROPERTY”.

Because in changing markets, clarity becomes incredibly valuable.

Talk soon,

Reading is helpful. Having a plan is better.

Book your free 30-minute Discovery Session and let’s build a strategy that fits your life.

7Wealth Pty Ltd ABN 44609210246 is a Corporate Authorised Representatives and is authorised throughCobalt AdvisersPty Ltd ABN 64 628 654 099 who is an Australian Financial Services Licensee 512550. 7Wealth Pty Ltd is a Credit Representative ofAustralian Finance GroupLtd ABN 11 066 385 822 (AFG) Australian Credit Licence 389087.

This blog contains information that is general in nature. It does not constitute financial or taxation advice. The information does not take into account your objectives, needs and circumstances. We recommend that you obtain investment and taxation advice specific to your investment objectives, financial situation and particular needs before making any investment decision or acting on any of the information contained in this document. Subject to law, Cobalt Advisers Pty Ltd nor their directors, employees or authorised representatives, do not give any representation or warranty as to the reliability, accuracy or completeness of the information; or accepts any responsibility for any person acting, or refraining from acting, on the basis of the information contained in this document.